Genetic scientists study human DNA to better understand medical conditions and how to treat diseases. But their research is often based on samples that don’t actually reflect the world’s population. Around 80 percent of the human DNA used in genetic studies is from people of European descent. This means that researchers are often unable to study and address conditions that affect global ethnicities.

In January 2019, Abasi Ene-Obong, a young tech engineer from Nigeria, founded 54gene with the aim of making gene studies more representative by increasing access to African genomic data—which currently accounts for less than 3 percent of all genetic data sets. After securing two rounds of funding, 54gene has gone on to complete a fully resourced biobank in Lagos, crucial to support academic research, drug development, and disease detection.

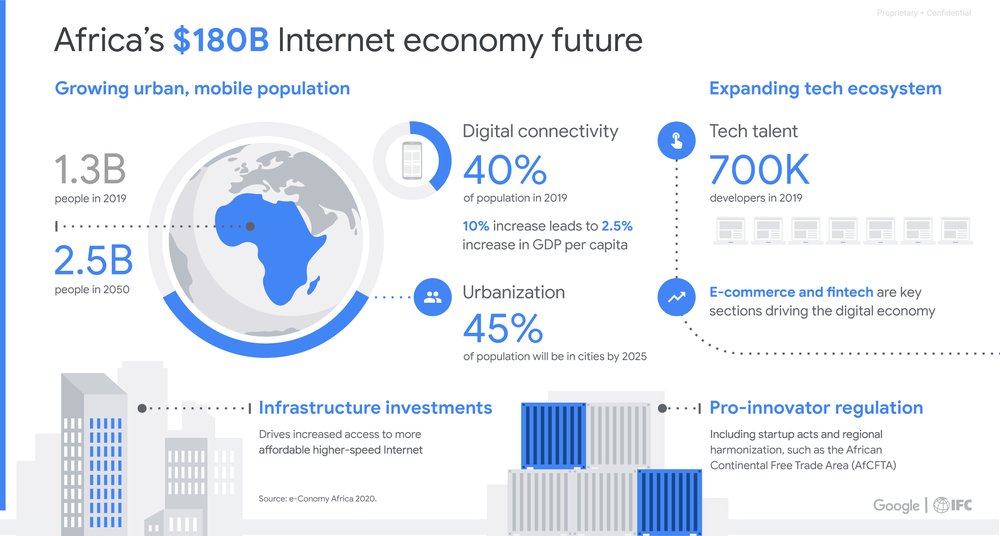

Ene-Obong’s story is just one example of how talented African entrepreneurs are creating new opportunities across the continent. As a new report from Google and the International Finance Corporation (IFC) shows, the startup ecosystem is helping drive Africa’s internet economy towards a projected value of $180 billion by 2025, or 5.2 percent of the continent’s GDP.

We collaborated on the report—titled ”e-Conomy Africa 2020: Africa’s $180 billion internet economy future”—to highlight the strengths and challenges of the internet economy today, and to better understand where it might go in the future. Here are some other things we learned.

Startups in Africa are progressing and reaching new milestones

According to Partech Ventures Africa, African tech startups reached a new milestone in 2019 with $2.02 billion of equity funding raised. That’s 74 percent more than in 2018, and represents an average deal size of $8.08 million.

At the forefront of the internet economy’s growth are startups in sectors like financial technology (fintech), e-commerce, health, e-logistics, e-mobility and food delivery. Fintech leads the way in terms of funding, receiving 54 percent of all African startup investment in 2019. This indicates high investor trust, which is significant given the sector’s important role serving unbanked and financially excluded Africans.

One example is the Nigerian digital payments and commerce platform Interswitch, which received $200 million in equity funding from Visa in 2019, as well an IFC investment of $10.5 million. These investments came at a time of big growth for the electronics payment market, and, as a result, Interswitch has helped transform the infrastructure of Nigeria’s banking system, while extending its services to 23 other countries.

E-commerce startups have also shown strong growth, thanks to improved digital payment services and a rise in mobile technology and payment channels. In 2019, e-commerce accounted for $134 million in funding across 30 deals–a 36 percent increase in the number of deals compared with 2018. With COVID-19-mandated lockdowns in countries across the continent, consumers have quickly gotten much more used to e-commerce, and their new online shopping behavior may well extend beyond the pandemic.

Young developer talent is shaping the future

The African developer scene boasts 700,000 professional software developers, many of them trained through university programs, others self-taught.

There’s an enormous amount of talent, but these developers need help to find jobs and take their ideas forward.

Coding classes, like those offered by Google, Decagon, Gebeya and others, are helping close knowledge and skills gaps, while professional communities continue to grow. There are more than 160 active Google Developer Groups and 200 Developer Student Clubs in Sub-Saharan Africa, offering training and support to help developers meet job requirements. And since its launch in 2018, theGoogle for Startups Accelerator Africa program has worked with 47 startups from 17 African countries—helping them develop products and build successful companies and products. One of the 2016 global accelerator graduates, Nigerian fintech startup Paystack, was recently acquired by Stripe for over $200 million.

IFC is also playing its part to advance digital skills development, making investments in regional startups and accelerators that cultivate tech talent. Gebeya—a company IFC supports in Ethiopia—has trained over 500 young software developers, most of whom are women, and is providing seed funding to 30 graduates to pursue their own digital ventures. IFC investee Flat6Labs is fostering tech entrepreneurship (and women entrepreneurs in particular) by directing early stage funding to startups in both Egypt and Tunisia.

Whether it’s helping startups grow, training developers or providing tools for small businesses, both Google and IFC are committing to bringing the benefits of technology to millions more people across this extraordinary continent. We invite you to read the report and learn more about the opportunities unfolding throughout Africa’s thriving internet economy.

{kind=link}